?2 Shaft - Konkola North (Vale/ARM) - Zambian Copperbelt (sitios de interés)

Descripción del sitio

RESOURCE BASE

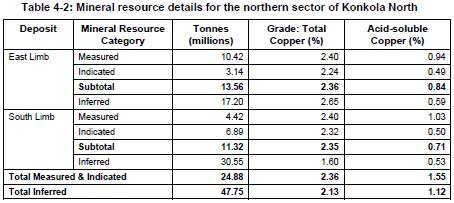

Northern Sector: Inferred 78.8Mt at 2.14% Cu (South & East Limb)

Southern Sector: Inferred 170Mt at 2.88% Cu (Area 'A' & Area 'A' Ext)

STATUS - CONSTRUCTION FASE

NORTHERN SECTOR MINE & CONCENTRATOR

• ARM and Vale approve release of new copper mine in Zambia

• Total project capital expenditure, in July 2010 terms, is US$380 million. Construction commenced in August 2010 with commissioning of the concentrator plant expected 27 months later. The mine is planned to reach full production in 2015.

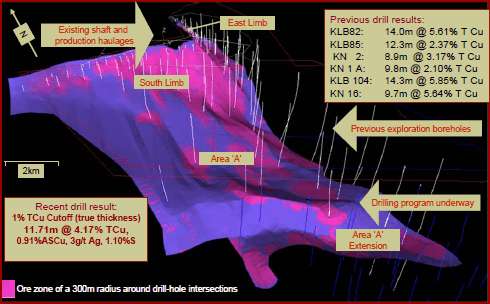

• The expected life of mine of Konkola North is 28 years. A further three year exploration programme to evaluate area “A”, which has potential to double the output to 100 000 tonnes copper per annum in concentrate is in progress. Initially, the South and East Limb Mines will be developed, after which the deeper, higher grade and wider reef areas will be mined.

• The mine’s throughput design is 2.5 mtpa of ore at an average mill head grade of 2.3% copper, yielding 45 000 tonnes of contained copper in concentrate to be toll smelted in Zambia.

OWNERSHIP - KONKOLA NORTH COPPER MINE

Konnoco Zambia Ltd

• 50% African Rainbow Minerals Ltd - ARM

• 50% Vale S.A.

• ZCCM-Investment Holdings Plc -ZCCM-IH has a buy-in right of either 15% or 20% with 5% thereof being a free carry

--------------------------------------------------------------

KONKOLA NORTH COPPER PROJECT (KNP)

March 2008 - EIAR

Mining the South Limb and the East Limb with dedicated concentrator

Use existing shaft and ramp from existing workings to 600m

Average thickness of orebody: 4m-5m

Life of Mine average on-mine (mining) cost: <US$1.10/lb

Mining fleet: contract operated, TEAL owned

Life of mine: +20 years

Capital required: US$160m

Copper production: 25,000 tpa

Use existing shaft and ramp from existing workings to 600m

Average thickness of orebody: 4m-5m

Life of Mine average on-mine (mining) cost: <US$1.10/lb

Mining fleet: contract operated, TEAL owned

Life of mine: +20 years

Capital required: US$160m

Copper production: 25,000 tpa

The Konkola North Copper Project is located within the greater Konkola area of the Zambian Copperbelt and consists of a single large scale mining licence covering an area of approximately 44 square kilometres. The development of this project is a high priority for the Company. In the opinion of RSG Global, the greater Konkola area represents one of the largest undeveloped copper resources in the world. Pursuant to a drilling program in excess of 47,000 metres, TEAL has identified inferred mineral resources of 78.8 million tonnes at 2.14% copper. This resource is contained within only the east and south limb areas of the project. Historic records and more recently drilled results relating to other areas of the project indicate a further inferred mineral resource of approximately 107 million tonnes at grades of 2.30% and 63 million tonnes at grades of 3.88% copper. See "Zambia – Copper Projects – Konkola North Copper Project – Mineral Resources". At the south limb, TEAL intends to focus initially on the development of a high-grade region of the deposit and re-equipping of the existing infrastructure, which includes a 423 metre vertical shaft, two ventilation shafts and three ore haulage levels. At the east limb, the Company is considering the sinking of a decline shaft to access the mineralization. The Konkola North Copper Project is adjacent to the existing Konkola Mine, owned by Konkola Copper Mines plc, which has existing operational mining infrastructure. The Konkola North Copper Project is subject to a buy-in right of up to 20% (including a 5% carried interest) by ZCCM Investments Holdings plc ("ZCCM-IH"), a company controlled by the Zambian Government.

Source: SKR EIAR ----------------------------------------------------------

Rothschild & Sons Limited on synergies with KCM past 2017

- Use of KCM Shaft No 3 for Konkola North

- Nchanga Tailings Leach Plant in relation to Mwambashi B

Konkola North was sold separately at the time of the privatisation of ZCCM and at the Relevant Date was owned by Teal Exploration and Mining. This company was floated on the Toronto Stock Exchange shortly afterwards.

Konkola North contains the Northern extension of the Konkola ore body. Prior to 1959 this deposit was exploited and there is still a shaft (No.2 Shaft) in existence. However,recommencement of production will require extensive development. In its report, IMCL has indicated that it may be cost efficient to develop this asset using a portion of KCM s existing Konkola infrastructure and, specifically, to use the No.3 Shaft once this becomes surplus to requirements following KDMPs development. If this approach were adopted then KCM could extract some of the economic value through:

- some kind of arrangement involving payment/royalty, NPI or access charge as consideration for the use of its assets; or

- a full or partial (joint venture) acquisition of the deposit which would allow it to extract some of the synergies.

- some kind of arrangement involving payment/royalty, NPI or access charge as consideration for the use of its assets; or

- a full or partial (joint venture) acquisition of the deposit which would allow it to extract some of the synergies.

However, we do not believe that even an aggressive buyer of KCM would have been likely to have placed any material value on this possibility at the Relevant Date because:

- at the time, any development of Konkola North remained uncertain;

- based upon the Listing Particulars of Teal (which were published shortly after the Relevant Date) there is no evidence to suggest that Teal was considering a development that would rely in any material way on KCM s infrastructure;

- IMCL s work has indicated that the development schedule for Konkola means that the shaft would only become available post 2017. We therefore suspect that any NPV benefit to Teal from its use would be more than offset by the NPV loss of the delay in Konkola North s development (albeit it could be used in a subsequent phase); and, more generally,

- based upon the Listing Particulars of Teal (which were published shortly after the Relevant Date) there is no evidence to suggest that Teal was considering a development that would rely in any material way on KCM s infrastructure;

- IMCL s work has indicated that the development schedule for Konkola means that the shaft would only become available post 2017. We therefore suspect that any NPV benefit to Teal from its use would be more than offset by the NPV loss of the delay in Konkola North s development (albeit it could be used in a subsequent phase); and, more generally,

- arrangements of this type, while often considered in the mining industry, are usually difficult to agree and it is quite common, even when considerable demonstrable synergies are available, for the value not to be realised.

Separately, Teal own the majority of the small Mwambashi B deposit. IMCL believes exploitation of this might be more logical if the ore was processed through the Nchanga Tailings Leach Plant. In its Listing Particulars Teal specifically identified the availability of nearby processing facilities as a means of reducing the capital expenditure of a development. We are not aware that at the Relevant Date any significant discussions had taken place regarding this approach and, furthermore, Teal had yet to conduct a Feasibility Study. Given these considerations and the project s relatively small scale we doubt a buyer would have attributed material value to the possibility of extracting value through third party processing of Mwambishi B material.